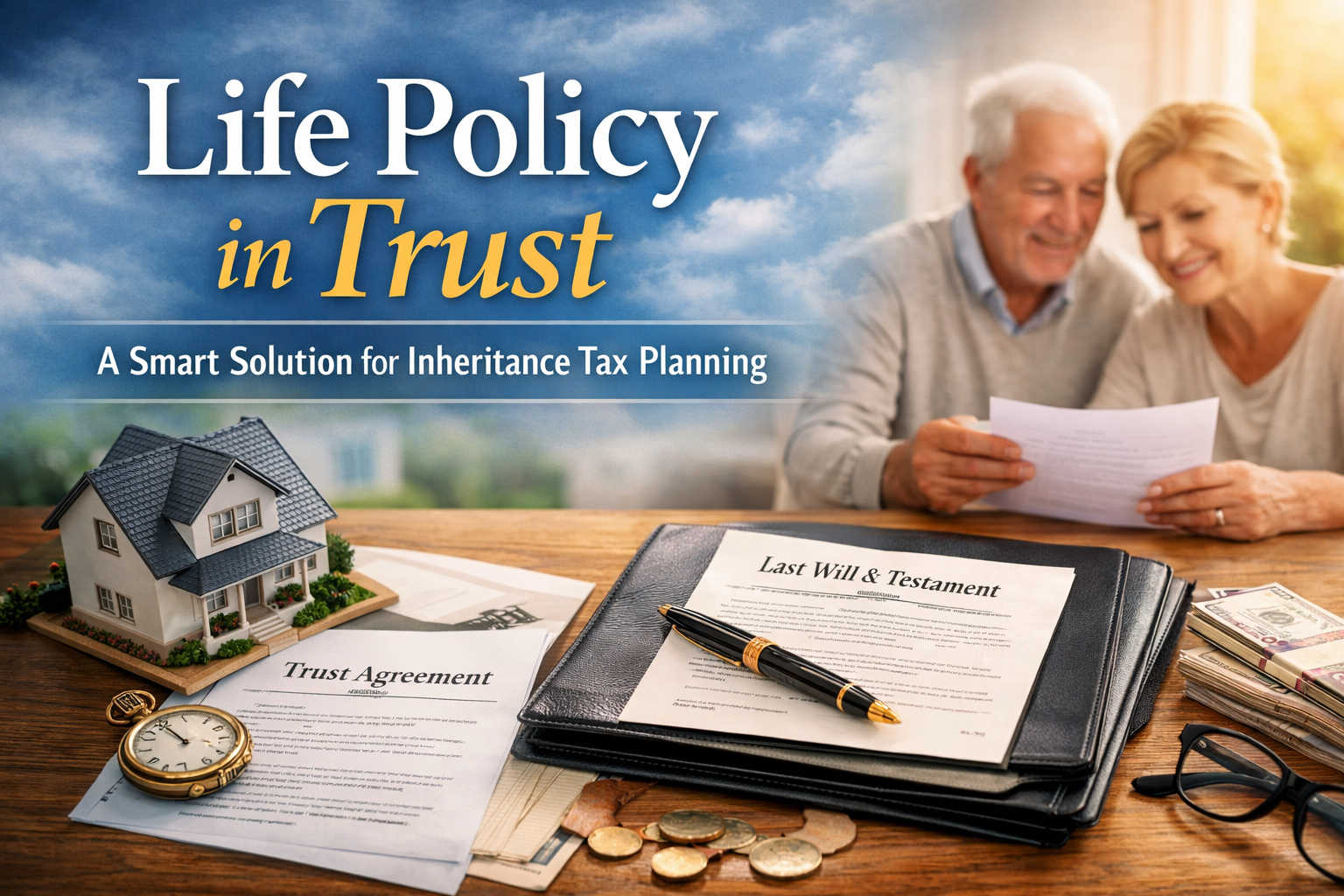

Life Policy in Trust for Inheritance Tax Planning in the UK

Inheritance Tax planning has become increasingly important for UK families, particularly

where wealth is tied up in residential and investment property. With property values rising steadily over the last two decades, many estates now exceed the available tax free allowances.

One of the most practical and widely used solutions is a life policy written in trust. This article explains how a life policy in trust works, whether there are trust charges, and how it can help families manage Inheritance Tax liabilities efficiently.

What Is a Life Policy in Trust?

A life policy in trust is a life insurance policy that is legally placed into a trust at the time it is taken out. Instead of the payout forming part of the deceased’s estate, the insurance proceeds are paid directly to trustees for the benefit of named beneficiaries.

This structure means:

- The payout does not increase the taxable estate

- The funds are not subject to Inheritance Tax

- The money is not delayed by probate

- Beneficiaries receive funds quickly

In simple terms, the insurance sits outside the estate for Inheritance Tax purposes.

Why Is This Important for Inheritance Tax Planning?

Inheritance Tax in the UK is charged at 40 percent on the value of an estate above the available allowances. For married couples or civil partners, this can be up to £1 million if the main residence passes to direct descendants.

However, many estates exceed this level, especially where:

- The family home has significantly increased in value

- There are buy to let properties

- There are additional investments

Inheritance Tax is generally payable within six months of death. If the estate is mainly property based, beneficiaries may need to sell assets quickly to fund the tax bill. This creates financial pressure and may result in properties being sold below market value.

A life policy in trust is designed to solve this liquidity problem.

Example: How a Life Policy in Trust Works

Consider a married couple with the following position:

- Family home valued at £1.4 million

- Investment property worth £600,000

- Savings and investments of £200,000

Total estate value: £2.2 million

Assuming full transferable allowances of £1 million, the taxable estate would be approximately £1.2 million.

At 40 percent, the estimated Inheritance Tax liability would be around £480,000.

Without planning, the executors would need to find £480,000 within six months. If the estate does not hold sufficient cash, a property may need to be sold quickly to raise funds.

Now consider the alternative:

The couple take out a joint life second death whole of life policy for £500,000 and write it into a discretionary trust for their children.

On the second death:

- The insurance company pays £500,000 directly to the trustees

- The payout does not form part of the estate

- The trustees use the funds to pay the Inheritance Tax

The family properties remain intact. There is no forced sale and no delay waiting for probate funds.

Are There Trust Charges?

A common concern is whether placing a life policy into trust creates additional tax charges.

In most standard Inheritance Tax planning arrangements, the answer is no.

When a new pure protection life policy is written into trust at inception, its value is negligible. Therefore:

- There is no immediate 20 percent entry charge

- There are typically no ten year periodic charges

- There are usually no exit charges

This is because the trust does not hold a valuable asset during lifetime. The policy only pays out on death and usually has little or no surrender value.

However, if an investment linked policy is used and builds up significant value during lifetime, the trust could fall within the relevant property regime and periodic charges may apply. For Inheritance Tax planning, protection only whole of life policies are normally used to avoid this issue.

Whole of Life vs Term Assurance

There are two common types of life cover used in estate planning.

Whole of life policies provide cover for life and are typically used to fund ongoing Inheritance Tax exposure.

Term assurance policies provide cover for a fixed period, for example seven years. They may be suitable where planning relates to covering the potential tax risk during the seven year survival period after a large gift.

For married couples, joint life second death policies are often used because Inheritance Tax generally arises on the second death.

Key Advantages of a Life Policy in Trust

A life policy in trust offers several benefits in UK estate planning:

- No Capital Gains Tax is triggered

- No assets need to be transferred

- No seven year survival requirement

- Funds are available immediately

- Probate delays are avoided

- Estate liquidity is protected

It does not remove the Inheritance Tax liability. Instead, it ensures that the tax can be paid without disrupting the family’s long term wealth.

Is a Life Policy in Trust Right for You?

A life policy in trust is particularly suitable where:

- The estate is property heavy

- There is limited cash available

- The client does not want to gift assets

- The Capital Gains Tax cost of transferring property is high

It should form part of a wider Inheritance Tax planning strategy that includes a properly drafted will, review of available allowances, and regular estate valuation updates.

For many UK families, especially those with valuable residential property, a life policy in trust is one of the most straightforward and effective tools available to protect wealth and preserve assets for the next generation.