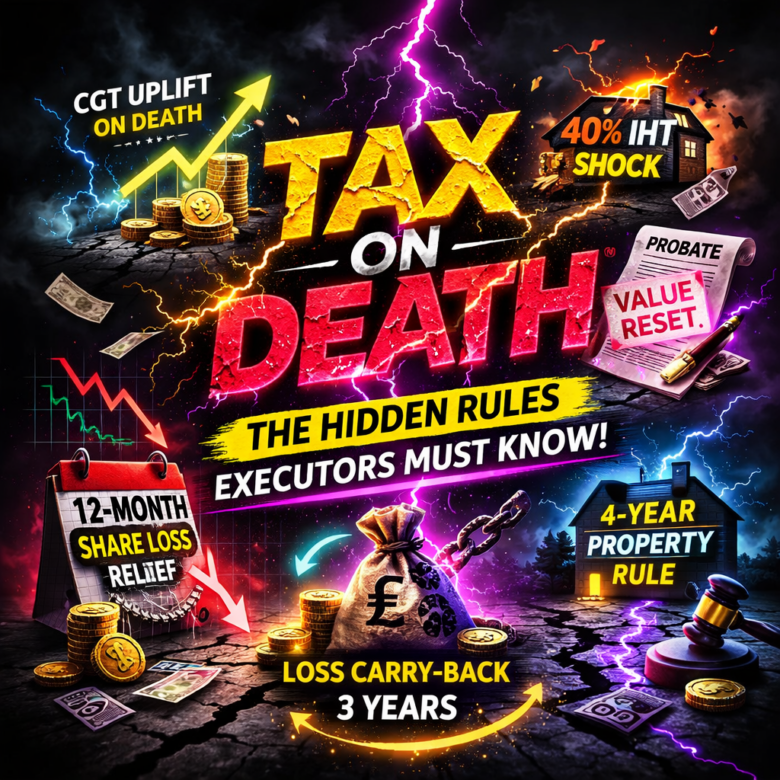

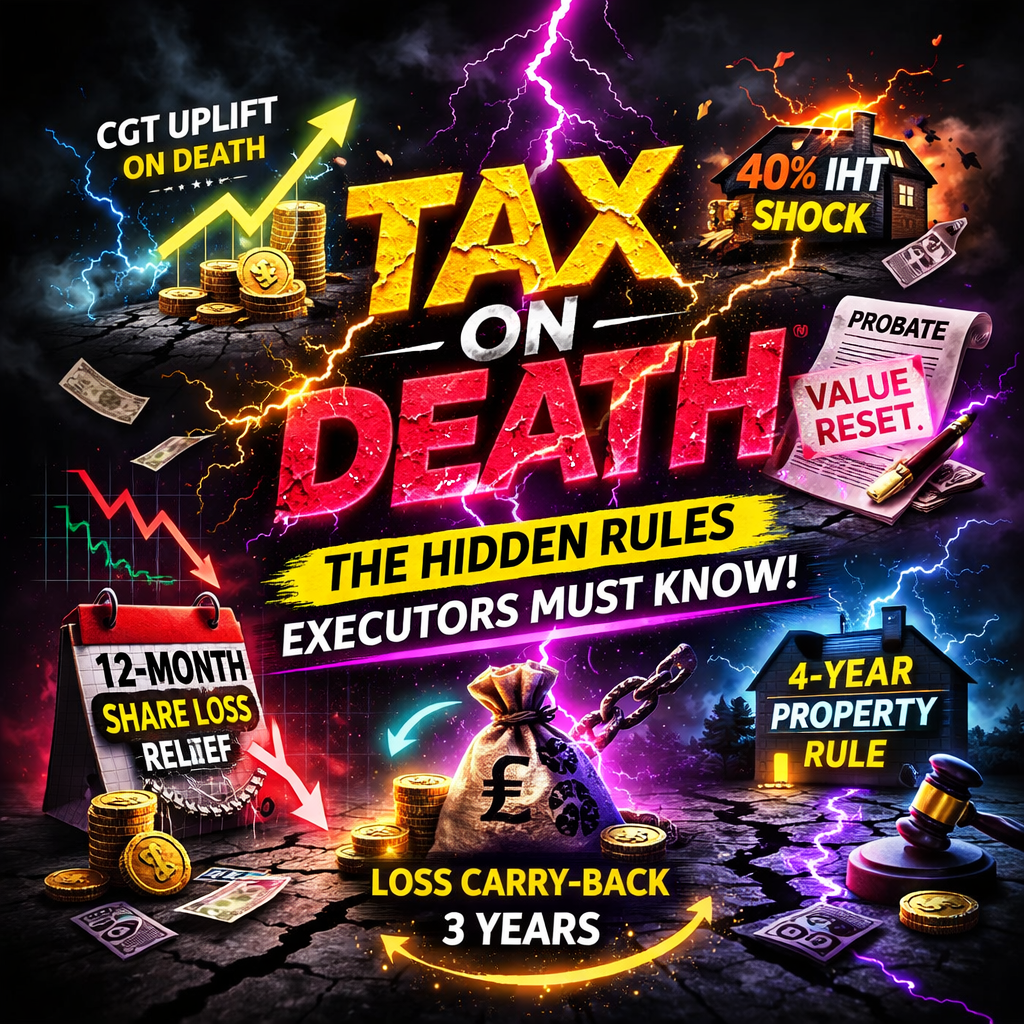

Navigating the Complexities of Tax on Death in 2026

When most people think about tax on death, they focus solely on Inheritance Tax (IHT). However, for executors and Personal Representatives (PRs), the tax position during estate administration is far more complex.

Beyond the 40% Inheritance Tax rate, there are critical Capital Gains Tax (CGT) reliefs,

loss carry-back provisions, probate value resets, share loss relief, and property loss relief rules that can significantly reduce the overall tax liability of an estate.

Understanding these HMRC rules on tax relief after death is essential for protecting the estate and maximising the inheritance received by beneficiaries.

1. Capital Gains Tax (CGT) Uplift on Death

One of the most important tax reliefs on death is the CGT uplift on death.

When an individual dies, their assets are automatically revalued to their market value at the date of death, known as the probate value. This creates a Capital Gains Tax uplift, meaning:

-

Any capital gains accumulated during the deceased’s lifetime are effectively erased.

-

Executors and beneficiaries receive assets with a new CGT base cost equal to the probate value.

This CGT uplift can eliminate significant Capital Gains Tax liabilities during estate administration.

Strategic Spousal Transfers Before Death

Under UK tax law, transfers between spouses or civil partners are treated as “no gain, no loss” for CGT purposes.

This creates a legitimate estate planning opportunity:

-

A spouse holding highly appreciated assets can transfer them to a terminally ill partner.

-

On death, the asset receives the CGT uplift to probate value.

-

The surviving spouse inherits the asset at the new base cost.

-

The asset can then be sold with little or no Capital Gains Tax.

Used correctly, this strategy can substantially reduce CGT exposure within a family estate.

2. Capital Loss Carry-Back After Death

If the deceased incurred capital losses, those losses do not have to be wasted.

Normally, Capital Gains Tax losses can only be carried forward. However, when a taxpayer dies, HMRC allows a three-year loss carry-back.

This means:

-

Capital losses in the tax year of death

-

Can be offset against capital gains from the previous three tax years

-

Potentially generating a tax refund paid into the estate

For executors handling estate administration, reviewing prior tax returns is essential to ensure no CGT loss carry-back relief is missed.

3. Inheritance Tax (IHT) Share Loss Relief – The 12-Month Rule

Market volatility after death can create a serious issue. If quoted shares fall in value after the date of death, the estate may pay Inheritance Tax on a higher probate value than the actual sale price.

To address this, HMRC provides IHT share loss relief.

How Share Loss Relief Works

-

Applies to quoted stocks and shares

-

Shares must be sold within 12 months of the date of death

-

Executors can elect to substitute the lower sale price for the probate value

-

This reduces the Inheritance Tax liability

Because IHT is charged at 40%, claiming share loss relief often produces a larger benefit than relying on Capital Gains Tax adjustments.

Important: The “All or Nothing” Rule

Executors must include all shares sold within the 12-month period in the claim.

-

Gains and losses are aggregated.

-

Profitable sales can reduce the benefit of loss-making sales.

Careful timing of share disposals is essential during estate administration.

4. Property Loss Relief – The Four-Year Rule

Similar relief applies to land and buildings, but the rules differ.

If property is sold for less than its probate value, executors may claim IHT property loss relief.

Key Property Loss Relief Rules

-

Property must be sold within four years of the date of death

-

All land sold within the first three years must be included in the claim

-

Property sold at a profit in year four can be excluded

-

The loss must exceed £1,000 or 5% of probate value (de minimis rule)

This four-year window gives executors more flexibility when managing estate property sales and Inheritance Tax exposure.

5. Deducting Estate Administration Costs for CGT

During estate administration, executors may deduct certain costs when calculating Capital Gains Tax.

These include:

-

Costs of establishing title

-

Professional executor fees

-

Legal costs related to asset sales

Under HMRC Statement of Practice SP02/04, Personal Representatives can use an approved sliding scale of allowable administration expenses instead of itemising every cost.

Using these HMRC-approved deductions can reduce the CGT payable on estate asset sales and simplify compliance.

6. Modern Assets: Cryptocurrency and Unlisted Shares

Not all assets qualify for share loss relief.

Quoted shares listed on recognised stock exchanges qualify for IHT share loss relief. However:

-

Unlisted private companies fall under separate business relief rules.

-

Cryptocurrencies (e.g., Bitcoin or Ethereum) are not treated as quoted shares by HMRC.

If crypto assets fall in value after death, executors may still face Inheritance Tax based on the original probate value, without access to the 12-month share loss relief.

This creates significant risk in estates holding digital assets.

Executor Checklist: Reducing Tax on Death and Capital Gains Tax

To minimise tax during estate administration, executors should:

✔ Obtain accurate probate valuations

✔ Monitor the 12-month (shares) and four-year (property) deadlines

✔ Review prior tax returns for loss carry-back opportunities

✔ Consider timing of asset sales carefully

✔ Apply HMRC-approved administration cost deductions

Final Thoughts: Tax Relief on Death Is Not Automatic

The UK tax system provides multiple Inheritance Tax and Capital Gains Tax reliefs on death, but they are not automatic.

Executors and Personal Representatives must actively claim:

-

CGT uplift benefits

-

Share loss relief

-

Property loss relief

-

Capital loss carry-back

Failure to elect for these reliefs can result in the estate paying substantially more tax than legally required.

Careful estate administration, awareness of HMRC rules, and proactive tax planning can preserve significant wealth for beneficiaries.